SEO Featured Snippet

Wealth Types Compared Online helps investors understand how liquid, tangible, intangible, digital, inherited, and self-made assets contribute to long-term financial success. Comparing each wealth category allows you to build a balanced portfolio, improve net worth, reduce financial risk, and create sustainable generational wealth.

Introduction

Building wealth isn’t simply about earning a high salary. True financial security comes from understanding how different types of wealth work together to grow your net worth over time. Many people focus only on income, while successful investors evaluate liquidity, ownership, diversification, and long-term appreciation before making financial decisions.

This guide explores Wealth Types Compared Online by explaining the strengths and weaknesses of every major asset category. Whether you’re just starting your financial journey or improving an existing portfolio, understanding these wealth types can help you make smarter investment decisions and protect your future.

What Are the Different Types of Wealth?

Wealth exists in many forms beyond cash sitting in a bank account. Some assets provide immediate spending power, while others generate appreciation over decades. Understanding these categories allows investors to build stronger financial foundations.

Understanding Generational vs Acquired Wealth

One of the biggest distinctions in personal finance is whether wealth is inherited or created.

Generational wealth refers to assets passed from one generation to another. These often include:

- Family businesses

- Investment portfolios

- Rental properties

- Land holdings

- Trust funds

- Stock portfolios

Families that consistently preserve assets over multiple generations benefit from compound growth, tax planning, and disciplined investing. Long-term trends show that successful families focus on preserving capital rather than simply increasing income.

Acquired wealth, on the other hand, is built through personal effort. It commonly comes from:

- Employment income

- Entrepreneurship

- Investing

- Real estate appreciation

- Business ownership

- Side businesses

Self-made investors generally experience greater financial flexibility because they develop strong money management habits while building their assets.

Which Is Better?

Neither type is automatically superior.

Inherited wealth provides an early financial advantage, while self-made wealth often creates stronger financial discipline. The most successful families combine both by preserving inherited assets while continuing to create new ones.

Tangible Versus Intangible Assets

Another important comparison involves physical assets versus intellectual assets.

Tangible Assets

Tangible assets have physical existence and measurable market value.

Examples include:

- Residential real estate

- Commercial property

- Gold and silver

- Vehicles

- Fine art

- Machinery

- Agricultural land

These assets often appreciate over long periods and provide stability during economic uncertainty.

Intangible Assets

Intangible assets don’t physically exist but may become even more valuable than physical property.

Examples include:

- Copyrights

- Patents

- Trademarks

- Intellectual property

- Brand recognition

- Royalties

- Software licenses

- Digital products

In today’s economy, intellectual property frequently produces recurring income without requiring additional physical investment.

Why Both Matter

A healthy personal balance sheet management strategy combines tangible and intangible assets.

For example:

- Property provides long-term equity.

- Intellectual property creates scalable income.

- Businesses generate cash flow.

- Investments build future appreciation.

Combining both categories reduces dependence on a single source of wealth and creates greater financial resilience.

How to Measure True Financial Wealth

Many people believe earning a six-figure salary automatically makes someone wealthy.

In reality, income and wealth are very different concepts.

Income measures how much money you earn.

Wealth measures what you actually own after subtracting liabilities.

Financial experts typically calculate wealth using a simple net worth formula:

Net Worth = Total Assets − Total Liabilities

Assets include:

- Cash

- Investments

- Retirement accounts

- Property

- Business ownership

- Vehicles

- Valuable collectibles

Liabilities include:

- Mortgages

- Student loans

- Credit card balances

- Auto loans

- Personal loans

Someone earning $300,000 annually with significant debt may have a lower net worth than someone earning $90,000 who consistently invests and avoids unnecessary borrowing.

Focus on Asset Retention

Long-term wealth comes from:

- Saving consistently

- Investing wisely

- Reducing unnecessary debt

- Allowing compound growth to work over decades

- Protecting existing assets

Experts emphasize sustainable asset retention rather than temporary increases in income because lasting financial independence depends on what you keep—not simply what you earn.

As your portfolio grows, reviewing your net worth annually helps identify weak areas, improve diversification, and ensure your financial strategy remains aligned with your long-term goals.

Why Is My Net Wealth Not Growing?

Many people earn a comfortable income yet feel their financial position never improves. The problem usually isn’t a lack of earnings—it’s how wealth is structured. Poor diversification, limited liquidity, excessive debt, and inefficient tax planning can quietly slow long-term financial growth.

Understanding these obstacles is the next step in mastering Wealth Types Compared Online and building a healthier financial future.

Overcoming Illiquid Investment Risks

Owning valuable assets is important, but not all assets are easy to access when you need cash. This is where illiquid investment risks become a major concern.

Illiquid assets include:

- Real estate

- Retirement accounts with withdrawal penalties

- Private equity

- Collectibles

- Land

- Certain business interests

Although these investments often appreciate over time, converting them into cash can take weeks or even months.

Why Illiquidity Can Be a Problem

Imagine facing an unexpected medical expense or business opportunity. If most of your wealth is tied up in property, you may struggle to access funds quickly without selling assets below market value.

Common consequences include:

- Forced asset sales

- High borrowing costs

- Missed investment opportunities

- Increased financial stress during emergencies

How to Reduce Illiquid Investment Risks

Financial experts recommend maintaining a balanced portfolio that combines long-term investments with easily accessible assets.

Practical strategies include:

- Keeping an emergency fund covering 3–6 months of expenses

- Holding cash or high-yield savings accounts

- Investing in marketable securities such as ETFs and stocks

- Reviewing asset liquidity every year

- Avoiding over-investment in a single property

A diversified liquidity strategy provides flexibility without sacrificing long-term growth.

The Hidden Impact of Inherited Wealth Tax Implications

Receiving family wealth is often viewed as purely beneficial, but taxes and legal obligations can reduce the value transferred to future generations.

Depending on your country’s regulations, inherited assets may involve:

- Estate taxes

- Capital gains taxes

- Probate costs

- Legal administration fees

- Property transfer expenses

Without proper planning, a significant portion of family wealth may never reach the next generation.

Financial Challenges Beyond Taxes

Inherited wealth can also create emotional and financial pressures.

Beneficiaries sometimes:

- Sell valuable assets too quickly

- Mismanage investments

- Spend inherited money without long-term planning

- Ignore diversification

These decisions can dramatically reduce family wealth within only one or two generations.

Managing Inherited Wealth Successfully

Professional wealth planners often recommend:

- Establishing family trusts

- Updating estate plans regularly

- Diversifying inherited investments

- Consulting tax professionals before major sales

- Creating long-term investment strategies instead of making emotional decisions

Careful planning helps preserve wealth while minimizing unnecessary tax liabilities.

Diagnosing Your Financial Portfolio Diversification

One of the most common reasons net wealth stagnates is poor diversification.

Many investors unknowingly place most of their money into one asset category.

Examples include:

- Buying multiple rental properties while ignoring stocks

- Investing only in cryptocurrency

- Keeping excessive cash that loses value to inflation

- Relying entirely on retirement accounts

This concentration increases financial risk because poor performance in one asset class can significantly affect overall wealth.

Signs Your Portfolio Needs Better Diversification

You may need to rebalance your portfolio if:

- One investment represents more than half your assets.

- Your returns fluctuate dramatically each year.

- You have limited access to liquid funds.

- Your investments all respond to the same market conditions.

Steps to Improve Financial Portfolio Diversification

Successful investors spread their capital across multiple asset classes.

A balanced portfolio may include:

- Cash reserves

- Domestic and international stocks

- Government and corporate bonds

- Real estate

- Precious metals

- Digital assets

- Retirement accounts

Regular portfolio reviews help ensure your investments remain aligned with your financial goals while reducing unnecessary risk.

Difference Between Liquid and Non-Liquid Wealth

One of the most important concepts discussed in Wealth Types Compared Online is understanding the difference between liquid and non-liquid wealth.

Although both contribute to your overall net worth, they serve very different financial purposes.

Liquid wealth consists of assets that can quickly be converted into cash with minimal loss in value.

Examples include:

- Cash

- Checking accounts

- High-yield savings accounts

- Publicly traded stocks

- Exchange-traded funds (ETFs)

- Money market funds

Non-liquid wealth includes assets that usually require time to sell.

Examples include:

- Residential property

- Commercial real estate

- Land

- Retirement accounts with restrictions

- Business ownership

- Fine art

- Collectibles

Understanding the balance between these categories is essential for long-term financial stability.

Why Liquid Wealth Matters in a Recession

During economic downturns, liquidity often becomes more valuable than high paper wealth.

Investors with sufficient liquid assets can:

- Cover living expenses without borrowing

- Avoid selling long-term investments at a loss

- Purchase discounted assets during market declines

- Handle emergencies with confidence

Those who lack liquidity may be forced to sell valuable assets at unfavorable prices.

Building a Strong Liquid Asset Allocation

Financial planners commonly recommend:

- Maintaining emergency savings

- Holding diversified stock investments

- Keeping short-term bonds available

- Avoiding excessive leverage

- Reviewing liquidity ratios annually

Strong liquid asset allocation improves financial resilience during uncertain economic conditions.

Is Real Estate Considered Net Wealth?

Yes.

Real estate is one of the largest contributors to personal net worth worldwide.

Your home’s value contributes to total assets, while the remaining mortgage counts as a liability.

For example:

- Home Value: $500,000

- Mortgage Balance: $250,000

- Home Equity: $250,000

Only the equity portion increases your personal net worth.

The Limitation of Real Estate

Although property often appreciates over decades, it is relatively illiquid.

Selling a house involves:

- Market timing

- Agent commissions

- Legal fees

- Closing costs

- Buyer negotiations

For this reason, homeowners should monitor long-term real estate equity growth while also maintaining accessible liquid savings.

How to Balance Physical and Paper Wealth

Successful investors rarely rely on one asset category alone.

Instead, they balance physical wealth with paper wealth.

Physical Wealth Includes

- Gold

- Silver

- Real estate

- Agricultural land

- Collectibles

- Commodities

Paper Wealth Includes

- Stocks

- Bonds

- Mutual funds

- ETFs

- Treasury securities

- Retirement investments

Each category offers different advantages.

Physical assets provide stability and inflation protection, while paper assets often deliver stronger long-term growth and easier diversification.

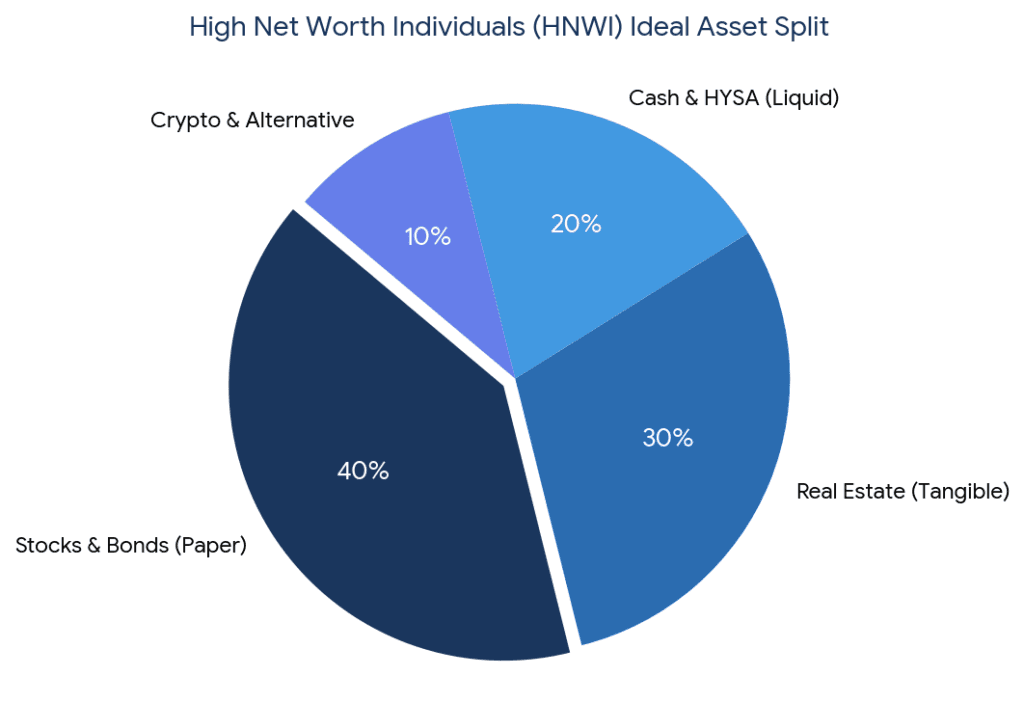

How High-Net-Worth Individuals Stay Balanced

Institutional investors and high-net-worth families typically maintain diversified allocations based on their financial goals, risk tolerance, and investment timeline.

Their systems often include:

- Broad stock market exposure

- Income-producing real estate

- Fixed-income securities

- Precious metals

- Alternative investments

- Cash reserves for opportunities and emergencies

Maintaining a balance between physical and paper wealth reduces volatility while creating multiple sources of long-term financial growth.

How Do Rich People Split Their Wealth?

Understanding Wealth Types Compared Online becomes even more valuable when you examine how wealthy individuals structure their portfolios. High-net-worth investors rarely depend on a single asset class. Instead, they spread their capital across multiple investments to balance growth, liquidity, and risk while preserving wealth for future generations.

Private Wealth Management Strategies Revealed

Professional wealth managers and family offices use disciplined asset allocation rather than chasing short-term market trends. Their goal is to create steady long-term growth while protecting capital during economic uncertainty.

Common Asset Allocation Strategies

Although allocations vary depending on age, goals, and risk tolerance, wealthy investors often diversify across:

- Public stocks and ETFs

- Government and corporate bonds

- Residential and commercial real estate

- Private businesses

- Cash reserves

- Precious metals

- Alternative investments

- Digital assets

Rather than trying to predict every market movement, they rebalance their portfolios regularly to maintain their desired asset mix.

Why Diversification Matters

Institutional private wealth management strategies focus on reducing risk by ensuring that one underperforming asset class does not significantly damage overall wealth.

Key principles include:

- Maintaining sufficient liquidity

- Investing across global markets

- Minimizing unnecessary taxes

- Reviewing portfolio performance annually

- Protecting assets through insurance and estate planning

This disciplined approach helps preserve wealth through changing economic cycles.

What Counts as Hidden Wealth Assets?

Many people calculate their wealth using only bank balances and property values. However, numerous valuable assets are often overlooked.

These hidden wealth assets may include:

- Intellectual property

- Royalties

- Patents

- Trademarks

- Private business equity

- Domain names

- Online businesses

- Licensing agreements

- Collectibles

- Cryptocurrency holdings

- Digital investment portfolios

These assets can significantly increase net worth while creating additional income streams.

Understanding Digital Asset Valuation

Digital assets have become an increasingly important part of modern portfolios.

Examples include:

- Cryptocurrency

- NFT intellectual property rights

- Revenue-generating websites

- Mobile applications

- Digital courses

- Subscription businesses

- Domain portfolios

Unlike traditional assets, digital investments can experience higher volatility. Proper valuation requires regular monitoring, market research, and risk management.

Can Digital Assets Build Generational Wealth?

Digital assets are no longer viewed as speculative investments alone. Many entrepreneurs are building businesses that generate recurring income and can be transferred to future generations.

Examples include:

- Software companies

- YouTube channels

- Membership websites

- E-commerce brands

- Digital publishing businesses

- Online education platforms

- Intellectual property portfolios

Benefits of Digital Wealth

Digital assets often offer:

- Global scalability

- Lower operating costs

- Passive income opportunities

- High profit margins

- Easier ownership transfer

Challenges to Consider

Despite their growth potential, digital assets carry risks such as:

- Rapid technological change

- Market volatility

- Cybersecurity threats

- Regulatory uncertainty

When combined with traditional investments, digital assets can strengthen a family’s long-term financial infrastructure while supporting future generations.

How to Compare My Wealth to Average

Comparing your financial position isn’t about competing with others—it’s about identifying strengths, weaknesses, and opportunities for improvement.

A complete wealth review should consider:

- Total net worth

- Liquid assets

- Retirement savings

- Investment portfolio

- Real estate equity

- Business ownership

- Debt obligations

- Digital assets

Best Ways to Track Different Wealth Types

Review each asset category separately rather than focusing only on income.

A practical tracking system includes:

- Updating your net worth every quarter

- Monitoring investment performance

- Reviewing debt reduction progress

- Measuring liquidity levels

- Tracking real estate appreciation

- Evaluating digital asset performance annually

Consistent tracking makes it easier to identify financial gaps and adjust your strategy before problems become significant.

Global Wealth Benchmark Matrix

The following comparison provides a quick overview of the major wealth categories discussed throughout this guide.

| Wealth Type | Primary Assets Included | Liquidity Speed | Growth Potential |

|---|---|---|---|

| Liquid Wealth | Cash, High-Yield Savings, Stocks | Instant to 3 Days | Moderate (Market Dependent) |

| Tangible Wealth | Real Estate, Gold, Physical Vehicles | Slow (Months) | High Long-Term Equity |

| Intangible Wealth | Intellectual Property, Patents, Brands | Variable | Exponential |

| Digital Wealth | Crypto, Domain Portfolios, Web Assets | Instant to Fast | High Risk / High Reward |

This benchmark demonstrates why successful investors combine multiple wealth types instead of relying on a single asset category. A balanced portfolio improves flexibility, reduces risk, and supports long-term financial growth.

Conclusion: Take Control of Your Financial Matrix

Comparing different forms of wealth reveals that true financial success extends far beyond earning a high income. Throughout this guide on Wealth Types Compared Online, we’ve explored how liquid, tangible, intangible, and digital assets each contribute to long-term financial security. We’ve also examined the importance of diversification, liquidity management, estate planning, and strategic asset allocation.

The most financially successful individuals don’t rely on one investment alone. Instead, they build diversified portfolios that combine growth assets with accessible cash reserves while continuously reviewing their net worth and investment performance. Whether you’re just beginning your wealth-building journey or refining an existing portfolio, understanding how each asset category works together is the key to lasting financial independence.

Start today by auditing your assets, measuring your liquidity, reviewing your diversification strategy, and identifying opportunities to strengthen your financial foundation. Small, consistent improvements today can create substantial wealth for generations to come.

Frequently Asked Questions (FAQs)

1. Which type of wealth is the easiest to convert into cash?

Liquid wealth—including cash, savings accounts, money market funds, and publicly traded stocks—is typically the fastest and easiest asset category to convert into cash.

2. Should I include retirement accounts when calculating my net worth?

Yes. Retirement accounts such as 401(k)s, pensions, and IRAs are valuable financial assets and should be included when calculating your overall net worth, even if withdrawal restrictions apply.

3. How often should I review my wealth portfolio?

Financial professionals generally recommend reviewing your complete portfolio at least once every six to twelve months, with quarterly check-ins for investment performance and asset allocation.

4. What is the biggest mistake people make when building wealth?

One of the most common mistakes is concentrating too much money in a single asset class while ignoring diversification, liquidity, and long-term financial planning.

“Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial, investment, or legal advice. Please consult a certified financial advisor before making any financial decisions.”

“Hi, I am Umer Hasib. I am a passionate blogger and content creator who loves exploring human psychology, social behaviors, and personal growth. Welcome to my inner space!”