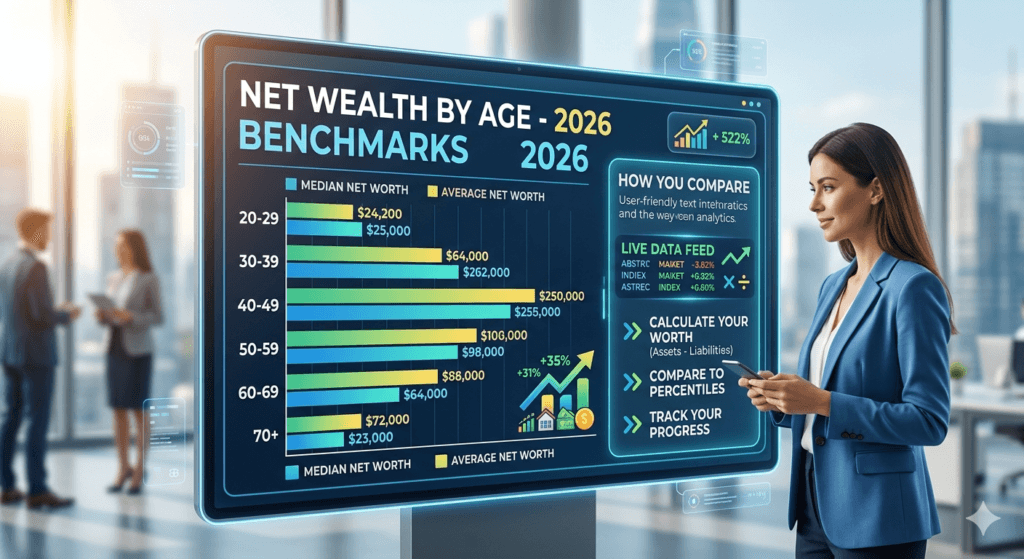

Featured Snippet:

Average Net Wealth by Age helps individuals compare their financial progress against national benchmarks. While average net worth figures can be skewed by ultra-wealthy households, median net worth provides a more realistic picture. Understanding both metrics allows you to evaluate your financial standing, set goals, and build long-term wealth confidently.

How Does My Net Worth Compare to the National Average?

Many people wonder whether they are ahead, behind, or exactly where they should be financially. Understanding Average Net Wealth by Age can provide valuable context, but it’s important to interpret the numbers correctly.

Why Is Median Net Worth Lower Than Average Net Worth?

One of the biggest misconceptions about wealth statistics is assuming that average and median values mean the same thing.

Average net worth is calculated by adding all household wealth together and dividing by the total number of households. However, this figure is heavily influenced by mega-wealthy individuals.

For example, if a billionaire enters a room with ten middle-class families, the average wealth of the room skyrockets, even though nobody else’s financial situation changed.

Median net worth tells a different story. It represents the middle point where half of households have more wealth and half have less. Because it is not distorted by extreme outliers, median net worth often provides a more accurate reflection of real-world financial conditions.

This distinction is crucial when analyzing household wealth distribution metrics and comparing your finances against national benchmarks.

Understanding Your True Financial Standing

Comparing yourself to others can create unnecessary financial anxiety.

Instead of focusing on whether you match national averages, evaluate your progress against realistic milestones:

- Emergency savings growth

- Debt reduction progress

- Retirement account contributions

- Investment portfolio expansion

- Home equity accumulation

The Federal Reserve Survey of Consumer Finances remains the gold standard for measuring wealth trends in America. Rather than obsessing over averages, use these benchmarks as guideposts to improve your financial health over time.

What Counts Toward Your Net Worth Calculation?

Before comparing yourself to age-based wealth benchmarks, you must understand how net worth is calculated.

How to Calculate Personal Net Wealth Accurately

Net worth is a simple formula:

Net\ Worth = Assets – Liabilities

Assets include:

- Cash savings

- Checking accounts

- Investment accounts

- Retirement savings

- Real estate

- Business ownership

- Vehicles and valuables

Liabilities include:

- Credit card balances

- Student loans

- Auto loans

- Mortgages

- Personal loans

A positive net worth means you own more than you owe. A negative net worth means debts exceed assets.

Liquid assets and retirement savings typically form the foundation of a healthy wealth-building strategy.

Is Home Equity Included in Net Worth Statistics?

Yes.

Home equity is a major component of net worth calculations.

Home Equity = Current Home Value − Remaining Mortgage Balance

Many households accumulate significant wealth through property appreciation over time.

Although home equity is considered illiquid wealth because it cannot be easily spent, it remains a critical part of total net worth profiles and national wealth statistics.

Navigating Your Early Career: How to Increase Net Wealth in Your 20s

Your twenties are less about having wealth and more about creating wealth-building habits.

The Power of Early Asset Accumulation

Time is the greatest wealth-building asset available.

Even modest investments can grow dramatically thanks to compound interest.

Young professionals who begin investing early often outperform higher earners who start later because compound growth has decades to work.

Key priorities include:

- Investing consistently

- Building emergency savings

- Maximizing employer retirement matches

- Avoiding lifestyle inflation

The relationship between compound interest and asset accumulation becomes increasingly powerful over long periods.

Overcoming Early Financial Hurdles

Most young adults face:

- Student loan debt

- Entry-level salaries

- Rising housing costs

- Limited investment capital

Strategies to overcome these challenges include:

- Creating a realistic budget

- Maintaining a healthy debt-to-income ratio

- Paying high-interest debt aggressively

- Developing multiple income streams

Small improvements early often create massive financial advantages later.

What Is the Average Net Worth for a 30 Year Old?

The thirties represent a transition from wealth-building foundations to meaningful asset growth.

Moving Past the Entry-Level Financial Phase

By age 30, many professionals begin experiencing:

- Career advancement

- Higher salaries

- Marriage and family formation

- Homeownership opportunities

Net worth percentiles by age become increasingly useful during this decade because wealth differences begin widening significantly.

Setting Foundation Targets for Thirtysomethings

Healthy financial milestones may include:

- 1× annual salary saved for retirement

- Fully funded emergency fund

- Consistent investment contributions

- Controlled consumer debt

Many financial planners use average 401(k) and IRA balances as reference points rather than strict requirements.

The goal is steady progress rather than perfection.

Mid-Life Check-In: How Much Net Wealth Should I Have by Age 40?

The forties are often characterized by peak earning potential combined with peak expenses.

Navigating Peak Earning and High-Expense Years

Common financial pressures include:

- Mortgage payments

- Childcare expenses

- College savings

- Aging parent responsibilities

Household wealth distribution metrics show substantial variation during this decade because life circumstances differ greatly.

The focus should be on increasing savings rates while maintaining financial flexibility.

Auditing Asset Allocation in Your 40s

Cash savings alone rarely generate enough growth.

A diversified investment portfolio may include:

- Stocks

- Bonds

- Real estate

- Retirement accounts

- Business investments

Systematic investment portfolio diversification helps balance growth opportunities and risk management.

The Pre-Retirement Panic: Am I Behind on Retirement Savings at 50?

Many people begin seriously evaluating retirement readiness during their fifties.

Benchmarking Your Fifty-Something Reality

Concerns about retirement are normal.

Questions often include:

- Have I saved enough?

- Will my money last?

- Am I running out of time?

Comparing your retirement accounts to average 401(k) and IRA balances can provide useful perspective, but personal circumstances matter far more than national averages.

Catch-Up Strategies for Late Starters

If you’re behind, consider:

- Maximizing retirement contributions

- Utilizing catch-up contribution limits

- Reducing unnecessary expenses

- Increasing investment allocations strategically

- Delaying retirement if necessary

Tax-advantaged accounts can significantly accelerate wealth accumulation during the final working years.

Golden Years Reality Check: What Is the Median Net Worth of a 60 Year Old?

The focus shifts from building wealth to preserving it.

Assessing Reassurance vs. High-Net-Worth Reality

Most retirees do not need multimillion-dollar portfolios to maintain financial stability.

There is an important difference between:

- Financial security

- Financial independence

- Luxury retirement

High-net-worth individual benchmarks can be interesting, but they should not define personal success.

De-risking Wealth Prior to Retirement

As retirement approaches, many investors gradually reduce risk exposure.

Common strategies include:

- Increasing bond allocations

- Building cash reserves

- Reducing concentrated stock positions

- Reviewing withdrawal plans

Protecting accumulated liquid assets and retirement savings becomes increasingly important.

What Is a Good Net Worth Before Retiring?

The answer depends entirely on lifestyle needs.

Defining Your Personal Financial Freedom Number

A retirement target should be based on annual expenses.

Many planners estimate:

Required Retirement Portfolio = Annual Expenses × 25

This framework helps estimate the assets needed to sustain retirement withdrawals.

Social Security benefits and pension income should also be incorporated into retirement planning calculations.

Factoring Inflation into Long-Term Planning

Inflation reduces purchasing power over time.

A retirement lasting 30 years could experience multiple economic cycles.

Defensive investment portfolio diversification can help preserve purchasing power and reduce long-term risks.

The Elite Tiers: How Much Money Does the Top 1% Have by Age?

Many readers are curious about wealth at the highest levels.

Decoding High-Net-Worth Individual Benchmarks

Top 1% wealth thresholds vary significantly by age.

Generally, these households possess:

- Large investment portfolios

- Significant real estate holdings

- Business ownership stakes

- Alternative investments

Net worth percentiles by age provide insight into how elite wealth compares to national averages.

The Anatomy of Ultra-High Net Worth Portfolios

The wealthiest households often allocate assets differently.

Common holdings include:

- Private businesses

- Commercial real estate

- Public equities

- Venture investments

- Income-producing assets

Home equity and real estate wealth frequently represent a substantial portion of elite portfolios.

Analyzing the Macro Picture: Average Retirement Account Balance by Age Group

Retirement savings remain one of the strongest indicators of long-term financial health.

Deep Dive into the Federal Reserve Survey of Consumer Finances

The Federal Reserve collects detailed data regarding:

- Household assets

- Liabilities

- Retirement accounts

- Income sources

These insights help economists evaluate overall consumer financial health across age groups.

The Reality of Modern Wealth Accumulation

Salary income alone often struggles to keep pace with:

- Housing inflation

- Healthcare costs

- Education expenses

Modern household wealth distribution metrics highlight the importance of investing and asset ownership rather than relying exclusively on earned income.

The Changing Landscape: Understanding Generational Wealth Gaps

Generational differences continue reshaping wealth statistics.

Why Millennials and Gen Z Face Different Hurdles

Younger generations encounter:

- Higher housing prices

- Increased student debt

- Delayed homeownership

- Rising living costs

Historical generational wealth gaps reveal how economic timing significantly affects wealth accumulation.

Inheritances and the Great Wealth Transfer

Over the coming decades, trillions of dollars are expected to transfer between generations.

This wealth transfer will influence:

- Homeownership rates

- Investment balances

- Net worth statistics

- Real estate wealth distribution

Future wealth patterns may look dramatically different from previous generations.

SERP Feature Optimization: Global Wealth Distribution & Percentile Data

Featured Snippet Target: Average Net Wealth By Age Reference Table

| Age Bracket | Median Net Worth | Average Net Worth |

|---|---|---|

| Under 35 | $40,000-$50,000 | $180,000-$220,000 |

| 35-44 | $130,000-$150,000 | $500,000-$600,000 |

| 45-54 | $240,000-$280,000 | $900,000-$1.1 Million |

| 55-64 | $350,000-$400,000 | $1.4-$1.8 Million |

| 65-74 | $400,000-$450,000 | $1.5-$1.9 Million |

Interactive Checklist: Assess Your Current Wealth Trajectory

Use this quick self-assessment:

- I know my current net worth.

- I track assets and liabilities monthly.

- I maintain an emergency fund.

- I contribute regularly to retirement accounts.

- I avoid high-interest consumer debt.

- I maintain diversified investments.

- I review financial goals annually.

- My savings rate increases with income.

The more boxes you can check, the stronger your wealth trajectory is likely to be.

Conclusion: Taking Practical Action to Build Your Net Wealth

Understanding Average Net Wealth by Age can help provide valuable financial perspective, but numbers alone never tell the complete story. Median net worth often reflects reality more accurately because average figures are heavily skewed by extremely wealthy households.

Key Takeaways on Net Worth Benchmarks

Remember:

- Median net worth is usually the most realistic benchmark.

- Wealth accumulation is highly personal.

- Consistency matters more than comparisons.

- Asset ownership drives long-term growth.

- Time remains your greatest investing advantage.

Your Next Financial Steps

Start by calculating your current net worth today. Review your assets, debts, retirement accounts, and investment holdings. Compare your progress against age-based benchmarks, identify opportunities for improvement, and create a realistic action plan. Financial success is not about keeping up with others—it is about making steady progress toward the life you want to build.

FAQs

1. What is considered a good net worth for my age?

A good net worth is one that is steadily growing, supports your financial goals, and exceeds your liabilities. Comparing against median net worth benchmarks often provides the most realistic measure.

2. Does retirement account money count toward net worth?

Yes. Retirement accounts such as 401(k)s, IRAs, pensions, and similar savings plans are included in net worth calculations.

3. Can I have a negative net worth in my twenties?

Absolutely. Many young adults have student loans and other debts that exceed assets. Negative net worth early in life is common and often temporary.

4. How often should I calculate my net worth?

Most financial experts recommend reviewing net worth quarterly or at least once per year to monitor progress and adjust financial goals.

“Hi, I am Umer Hasib. I am a passionate blogger and content creator who loves exploring human psychology, social behaviors, and personal growth. Welcome to my inner space!”