SEO Featured Snippet:

Strategies to Increase Net Worth involve increasing your assets while reducing liabilities through smart investing, debt elimination, cash flow optimization, and long-term wealth planning. By consistently applying proven financial habits, automating investments, and focusing on appreciating assets, anyone can build sustainable wealth and significantly improve their net worth over time.

Calculate Your Net Worth Instantly

Before exploring these Strategies to Increase Net Worth, use the calculator below to determine your current net worth. Simply enter your assets and liabilities to see where you stand financially.

Introduction

Building wealth is not about earning the highest salary; it is about keeping, growing, and protecting your money over time. Many individuals earn substantial incomes yet struggle to increase their net worth because they fail to manage assets and liabilities effectively.

The most successful wealth builders follow proven Strategies to Increase Net Worth that focus on financial discipline, smart investments, debt reduction, and continuous wealth preservation. This comprehensive guide explains how to expand your wealth systematically and create lasting financial security.

Understanding the Core Metrics of Wealth Expansion

The Mathematical Baseline: Breaking Down the Net Worth Formula

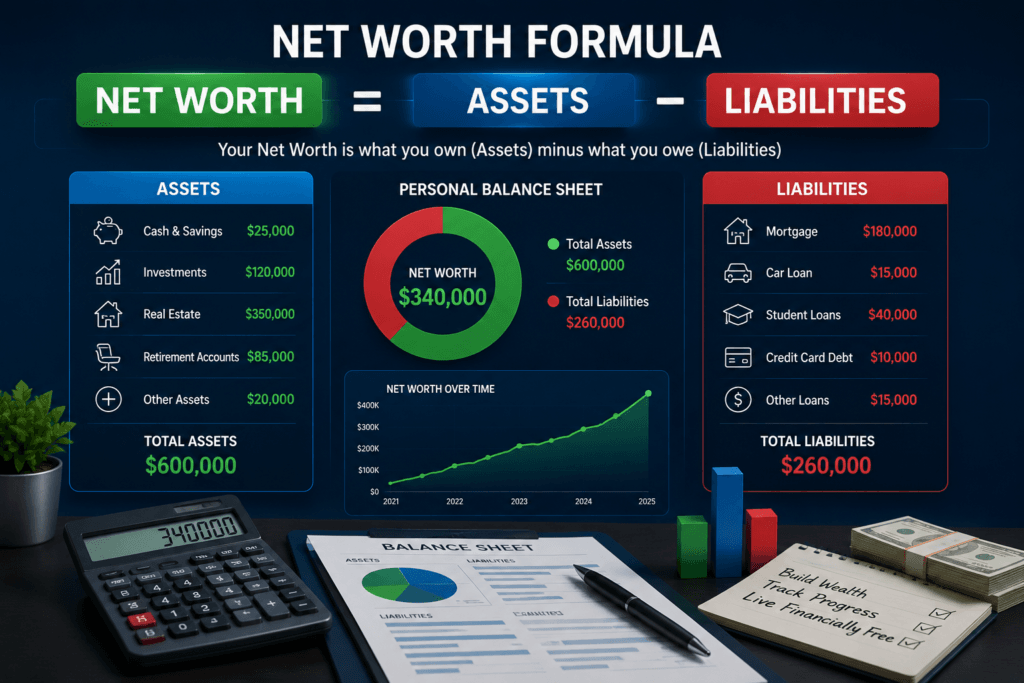

Net worth is calculated using a simple formula:

Net Worth = Total Assets – Total Liabilities

Assets include investments, savings, property, retirement accounts, and business ownership. Liabilities include mortgages, personal loans, credit card balances, and other debts.

Understanding this formula is the first step toward increasing wealth because every financial decision either raises assets or increases liabilities.

Personal Balance Sheet Management: Identifying What You Own vs. What You Owe

A personal balance sheet helps visualize your financial position.

Assets may include:

- Cash savings

- Stocks and ETFs

- Retirement accounts

- Real estate

- Businesses

Liabilities may include:

- Credit card debt

- Student loans

- Car loans

- Mortgages

Tracking both categories monthly allows you to identify areas for improvement.

Demystifying Liquid Net Worth Calculation vs. Fixed Assets

Liquid net worth measures assets that can quickly be converted into cash.

Examples include:

- Cash

- Savings accounts

- Brokerage investments

Fixed assets include:

- Real estate

- Vehicles

- Business ownership

Both metrics matter, but liquid net worth provides a clearer picture of short-term financial flexibility.

Shifting Mindsets from High Income to Wealth Accumulation

Why High Salaries Don’t Automatically Equal a High Net Worth

Many high earners remain financially vulnerable because spending rises with income.

Wealth is created when income exceeds expenses consistently and the difference is invested into appreciating assets.

Smart Financial Habits for Millionaires You Can Adopt Today

Common millionaire habits include:

- Living below their means

- Investing consistently

- Avoiding unnecessary debt

- Tracking expenses

- Prioritizing long-term goals

These habits create lasting financial momentum.

Overcoming Lifestyle Creep to Protect Your Capital Growth

Lifestyle creep occurs when spending increases every time income rises.

To prevent this:

- Increase investments before increasing spending

- Set financial targets

- Maintain a fixed savings percentage

This ensures income growth translates into wealth growth.

Laying the Foundation with Defensive Financial Planning

Establishing a Bulletproof Emergency Fund Allocation

An emergency fund should cover:

- 3–6 months of expenses for employees

- 6–12 months for entrepreneurs or freelancers

This protects investments from being liquidated during unexpected events.

Mitigating Risk to Prevent Net Worth Erosion During Market Downturns

Risk management includes:

- Diversification

- Insurance coverage

- Emergency reserves

- Asset allocation strategies

These measures reduce the impact of financial shocks.

Budgetary Restructuring Techniques to Plug Hidden Cash Leaks

Review monthly expenses and identify:

- Unused subscriptions

- Impulse purchases

- Excessive dining expenses

- High-interest debt payments

Redirecting these funds toward investments accelerates net worth growth.

Optimizing Your Cash Flow for Maximum Investment Power

Radical Maximizing Disposable Income to Fund Your Asset Purchases

The greater your disposable income, the greater your investing power.

Methods include:

- Negotiating salaries

- Developing side income

- Reducing recurring expenses

- Increasing productivity

Implementing an Automated Savings Mechanism to Remove Human Error

Automation eliminates emotional decision-making.

Set up:

- Automatic savings transfers

- Investment contributions

- Retirement account funding

Consistency beats occasional large investments.

Practical Ways to Grow Personal Capital Through Strict Margin Control

Margin control means ensuring expenses remain significantly lower than income.

Maintain:

- Spending plans

- Monthly financial reviews

- Investment targets

This creates sustainable wealth accumulation.

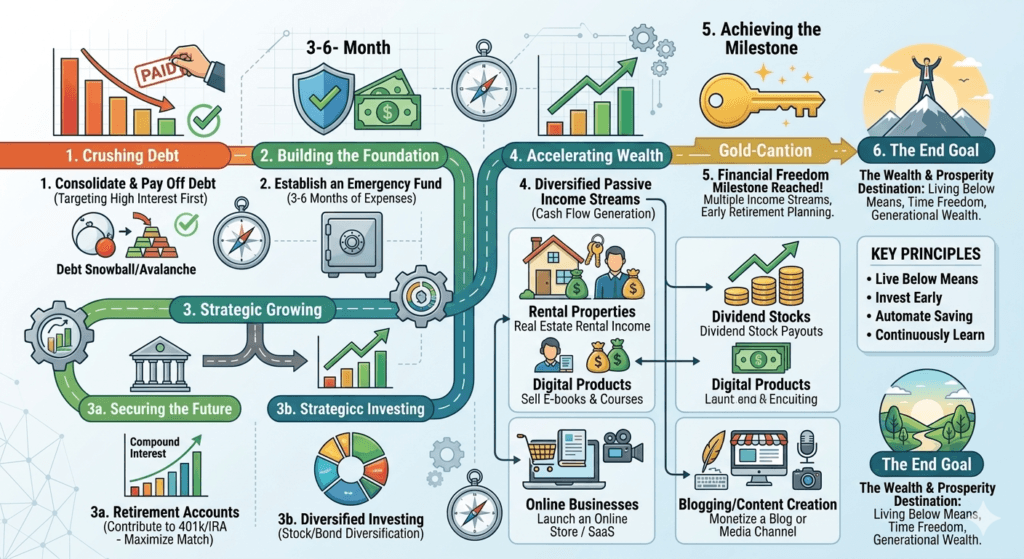

Aggressive Liability Reduction Strategies

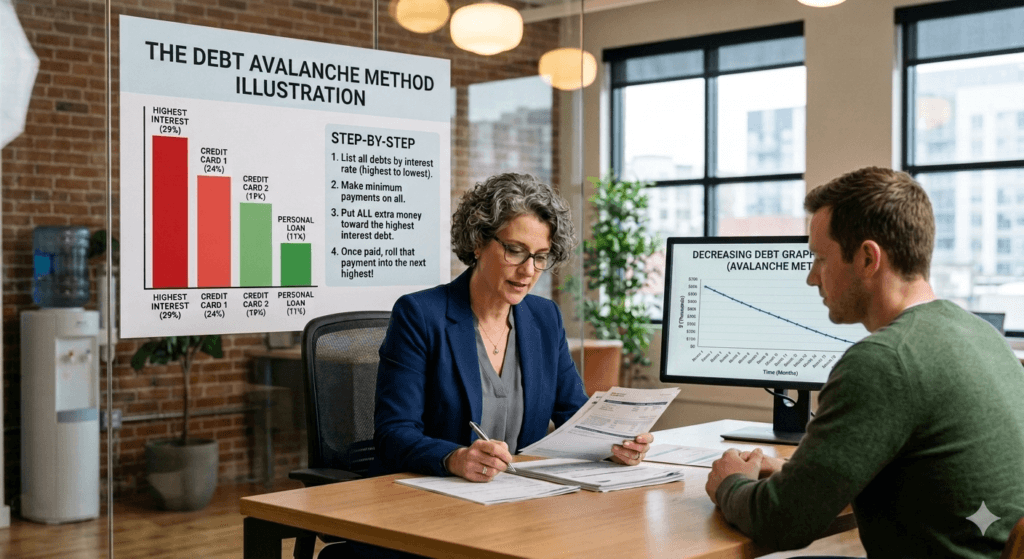

Dismantling Toxic High-Interest Commitments via the Debt Avalanche Method

The Debt Avalanche Method focuses on paying off debts with the highest interest rates first.

Benefits include:

- Faster interest savings

- Improved cash flow

- Accelerated wealth growth

The Fast Track to Reducing Consumer Debt Liabilities

Consumer debt often includes:

- Credit cards

- Personal loans

- Buy-now-pay-later services

Eliminating these liabilities increases net worth immediately.

Good Debt vs. Bad Debt: When to Leverage Liabilities Intentionally

Good debt may generate future value, such as:

- Business financing

- Real estate investments

- Educational investments

Bad debt funds consumption without generating returns.

Unleashing the Power of Exponential Compound Interest

Compound Interest Optimization: The Engine of Long-Term Wealth

Compound interest allows earnings to generate additional earnings.

genui{“math_block_widget_always_prefetch_v2”:{“content”:”A=P\left(1+\frac{r}{n}\right)^{nt}”}}

The earlier you start investing, the greater the compounding effect becomes.

The Timeline Factor: How Starting Early Drastically Changes the Wealth Curve

A person investing at age 25 can accumulate significantly more wealth than someone starting at age 40, even if total contributions are lower.

Time is the most valuable wealth-building asset.

Visualizing the Curve: How Small Actions Snowball Over 10, 20, and 30 Years

Consistent investing creates exponential growth:

- 10 years: Moderate growth

- 20 years: Significant acceleration

- 30 years: Massive wealth accumulation

Small monthly investments can become substantial portfolios.

Maximizing Tax-Advantaged Investment Vehicles

Strategic Contributions to Tax-Advantaged Retirement Accounts

Tax-advantaged accounts reduce current taxes while boosting long-term growth.

Examples include:

- Retirement plans

- Pension schemes

- Tax-deferred investment accounts

Claiming Your Free Money: Exploiting the Employer-Sponsored 401k Match

When employers match retirement contributions, employees receive an immediate return on investment.

Always prioritize capturing the full employer match whenever possible.

Advanced Net Wealth Tax Planning to Keep More of Your Gains

Effective tax planning may involve:

- Capital gains strategies

- Tax-loss harvesting

- Retirement account optimization

Keeping more of what you earn accelerates wealth creation.

Strategic Allocation into Appreciating Asset Classes

Distinguishing Between Appreciating Assets vs Depreciating Assets

Appreciating assets may include:

- Stocks

- Real estate

- Businesses

- Intellectual property

Depreciating assets include:

- Most vehicles

- Electronics

- Luxury consumer goods

Focus spending on assets that grow in value.

Building Out a Robust Asset Allocation Framework

A balanced portfolio may contain:

- Equities

- Bonds

- Real estate

- Alternative investments

Diversification improves risk-adjusted returns.

The Core Pillars of Modern Wealth: Stocks, Bonds, and Specialized Vehicles

Successful investors combine multiple asset classes to reduce volatility and improve long-term growth.

Harnessing Real Estate for Net Worth Acceleration

Multi-Generational Wealth: Real Estate Equity Building Tactics

Real estate builds wealth through:

- Property appreciation

- Rental income

- Mortgage principal reduction

Over time, equity accumulation significantly boosts net worth.

Residential vs. Commercial Real Estate: Which Scales Net Worth Faster?

Residential properties offer accessibility and stability.

Commercial properties often provide:

- Higher cash flow

- Greater scalability

- Larger appreciation potential

Each investor should choose based on experience and risk tolerance.

Leveraging Market Cycles to Acquire Underpriced Property

Buying during market downturns often creates opportunities for long-term gains and equity growth.

Constructing a High-Performance Paper Asset Portfolio

The Hands-Off Approach: Diversified Index Fund Investing

Index funds provide:

- Broad market exposure

- Lower fees

- Long-term growth potential

They remain one of the most effective wealth-building tools.

Identifying and Selecting High-Yield Investment Vehicles

Investors should evaluate:

- Dividend-paying stocks

- REITs

- Bonds

- Income-focused ETFs

Diversification remains essential.

Avoiding Portfolio Decay with a Regular Portfolio Rebalancing Strategy

Rebalancing ensures your portfolio maintains its intended risk profile and investment objectives.

Creating and Scaling Passive Income Infrastructure

Passive Income Streams Generation: Making Your Money Work 24/7

Examples include:

- Rental properties

- Dividend portfolios

- Royalties

- Digital products

Passive income accelerates wealth accumulation.

Automatic Wealth Accumulation Through Capital Gains Reinvestment Plans (DRIPs)

Dividend Reinvestment Plans automatically purchase additional shares using dividends, increasing compounding power.

Digital Real Estate and Modern Cash-Flow Assets

Digital assets include:

- Blogs

- Websites

- Online courses

- Subscription businesses

These assets can generate recurring revenue with relatively low operating costs.

Advanced Frameworks to Accelerate Financial Independence

Accelerating Financial Independence: Lessons from the FIRE Movement

FIRE stands for Financial Independence, Retire Early.

Core principles include:

- High savings rates

- Intentional spending

- Aggressive investing

Roadmap Checklist: Actionable Blueprints on How to Build Wealth Fast

- Eliminate high-interest debt.

- Build an emergency fund.

- Automate investing.

- Diversify assets.

- Track net worth monthly.

Shifting from Accumulation Phase to Long-Term Wealth Preservation

As wealth grows, preservation becomes increasingly important through diversification, insurance, and tax planning.

Auditing and Tracking Your Financial Velocity

Setting Up Your Master Tracking Net Worth Spreadsheet

Track:

- Assets

- Liabilities

- Monthly growth

- Investment performance

Monitoring progress improves accountability.

Key Performance Indicators (KPIs) for Checking Your Improving Personal Net Value

Important KPIs include:

- Savings rate

- Debt-to-income ratio

- Investment return rate

- Net worth growth percentage

Monthly vs. Quarterly Reviews: Finding Your Financial Rhythm

Monthly reviews improve awareness while quarterly reviews provide strategic direction.

A combination of both often works best.

Protecting Your Wealth Architecture Against Threats

Securing the Right Insurance Policies to Shield Accumulated Assets

Key policies may include:

- Health insurance

- Life insurance

- Disability insurance

- Property insurance

Insurance prevents catastrophic losses.

Asset Protection Trusts and Legal Frameworks for High Earners

Advanced asset protection structures may help preserve wealth from legal and financial risks.

Professional guidance is recommended.

Inflation-Proofing Your Portfolio to Maintain Purchasing Power

Invest in assets that historically outpace inflation, including:

- Equities

- Real estate

- Certain commodities

Protection against inflation preserves long-term wealth.

The Lifelong Education of High Net Worth Individuals

Continuous Financial Literacy: Books, Mentors, and Market Research

The wealthiest individuals continue learning throughout their lives.

Knowledge compounds just like money.

Embracing Calculated Risks While Avoiding Get-Rich-Quick Pitfalls

Successful investors evaluate risk carefully rather than chasing unrealistic returns.

Sustainable wealth requires patience.

Networking and Surrounding Yourself with Growth-Oriented Peers

Your environment influences financial behavior.

Building relationships with ambitious and knowledgeable individuals can improve decision-making and opportunities.

Conclusion: Your Actionable Roadmap to Sustainable Wealth

Increasing wealth is not about finding the perfect investment or timing the market flawlessly. The most effective Strategies to Increase Net Worth focus on balancing aggressive debt reduction with disciplined asset acquisition, automated investing, smart tax planning, and long-term wealth preservation.

By consistently increasing assets, minimizing liabilities, optimizing cash flow, and protecting what you build, you create an unbreakable financial foundation capable of growing through changing economic conditions.

Start today by auditing your liabilities, calculating your current net worth, creating a tracking spreadsheet, and implementing one new wealth-building habit this week. Small actions repeated consistently can transform your financial future.

Frequently Asked Questions (FAQs)

1. What is the fastest way to increase net worth?

The fastest approach combines eliminating high-interest debt, increasing savings rates, and consistently investing in appreciating assets such as stocks and real estate.

2. How often should I calculate my net worth?

Most financial experts recommend calculating net worth monthly or quarterly to accurately monitor financial progress.

3. What percentage of income should be invested to build wealth?

While individual circumstances vary, investing 15%–25% of income consistently is a common target for long-term wealth growth.

4. Can someone with an average income build a high net worth?

Yes. Consistent investing, disciplined spending, debt management, and long-term compounding can help average earners build substantial wealth over time.

“Hi, I am Umer Hasib. I am a passionate blogger and content creator who loves exploring human psychology, social behaviors, and personal growth. Welcome to my inner space!”