SEO Featured Snippet

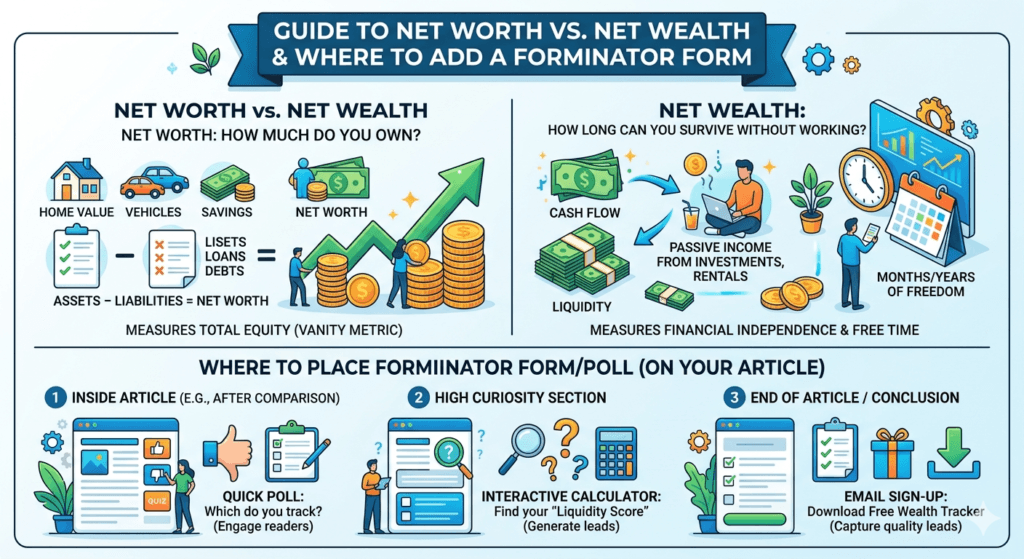

Net Worth vs Net Wealth is the difference between calculating what you own today and understanding your long-term financial freedom. Net worth measures assets minus liabilities, while net wealth includes liquidity, income potential, financial stability, and sustainable wealth-building strategies that support lifelong financial security.

Introduction

Money influences almost every decision we make, yet many people still feel financially insecure despite checking their bank accounts or investment portfolios every day. Watching account balances rise and fall can create unnecessary stress because those numbers don’t always reflect genuine financial security.

When discussing Net Worth vs Net Wealth, the confusion becomes even greater. Many assume both terms mean exactly the same thing, but they measure different aspects of financial health.

Your net worth is a snapshot of today’s financial position. Your net wealth tells a much broader story about financial independence, cash flow, long-term sustainability, and your ability to maintain your lifestyle regardless of economic uncertainty.

If your financial tracking focuses only on numbers that fluctuate with the stock market or property prices, you may be measuring temporary success instead of lasting financial freedom.

Why Tracking Net Worth Causes Financial Anxiety

Many people become emotionally attached to their net worth because financial apps update values daily. While tracking assets is helpful, constantly monitoring changing numbers often creates unnecessary anxiety.

Why Does My Net Worth Keep Changing?

Your net worth changes because your assets are constantly being revalued.

Common reasons include:

- Stock market volatility

- Capital appreciation of investments

- Capital depreciation during market corrections

- Real estate price fluctuations

- Business valuation changes

- Currency exchange movements

For example, if your investment portfolio gains 8% in one month, your net worth increases without you earning additional income. Likewise, a market correction can reduce your paper wealth overnight.

This doesn’t necessarily mean your financial situation has improved—or worsened.

Understanding this difference helps reduce emotional reactions to short-term market movements.

Moving Beyond the High Net Worth Individual Threshold

Many people chase the High Net Worth Individual (HNWI) label because it sounds prestigious.

However, reaching an arbitrary financial threshold does not automatically create financial freedom.

Someone with millions invested in businesses or property may still struggle with:

- Cash flow shortages

- High monthly debt payments

- Expensive lifestyles

- Limited liquidity

Instead of focusing solely on becoming a high-net-worth individual, focus on building financial independence where your assets consistently generate reliable income.

True wealth creates options—not stress.

How to Explain Net Wealth to Beginners

For beginners, the simplest explanation is this:

Net Worth = What you own minus what you owe.

Net Wealth = Your overall financial strength, including liquidity, income generation, financial flexibility, and future sustainability.

Think of your personal balance sheet like this:

Assets

- Cash

- Savings

- Investments

- Real estate

- Business ownership

- Vehicles

- Retirement accounts

Liabilities

- Mortgage

- Student loans

- Credit cards

- Personal loans

- Business debt

Subtract liabilities from assets to calculate net worth.

Then ask additional questions:

- Can these assets generate income?

- Can they easily be converted into cash?

- Will they support retirement?

Those answers determine your real net wealth.

Is Net Worth the Same as Net Wealth? The Core Differences

Although the terms are often used interchangeably, they are not identical.

Net worth measures financial position.

Net wealth measures financial resilience.

Total Gross Asset Liability vs. Real Equity

Many people focus on total assets without considering liabilities.

Suppose you own:

- $1,500,000 in property

- $400,000 in investments

- $150,000 in savings

Total assets equal $2,050,000.

But if you owe:

- $1,400,000 mortgage

- $300,000 business loans

Your real equity is only $350,000.

Another important distinction is liquidity.

A person may have:

- High total wealth

- Low liquid net worth

Liquid net worth includes assets that can quickly become cash without major losses.

Examples include:

- Cash

- Savings

- Money market funds

- Publicly traded stocks

Why Do Financial Planners Use Net Wealth?

Professional financial planners rarely focus only on asset totals.

Instead, they evaluate:

- Cash flow

- Financial flexibility

- Income sustainability

- Retirement readiness

- Socioeconomic status measurement indicators

- Asset quality

- Tax efficiency

Net wealth provides a broader picture because it measures how effectively assets improve your life rather than simply increasing paper value.

Comparison Table: Net Worth vs. Net Wealth

| Feature | Net Worth | Net Wealth |

|---|---|---|

| Definition | Assets minus liabilities | Overall financial health and freedom |

| Main Focus | Current balance sheet | Long-term financial security |

| Liquidity Level | May include illiquid assets | Strong emphasis on liquidity |

| Core Metric | Equity value | Financial independence |

| Income Consideration | Limited | Strong focus on passive income |

| Retirement Planning | Helpful | Essential |

| Cash Flow | Often ignored | Major consideration |

| Financial Stability | Snapshot | Long-term sustainability |

Can You Have a High Net Worth But Low Wealth?

Absolutely.

Many successful professionals experience this situation.

Their assets look impressive, but they lack financial flexibility.

The Trap of Illiquid Private Equity Holdings

Business owners often accumulate significant wealth through company ownership.

However, illiquid private equity holdings cannot always be sold quickly.

You may own a business worth $5 million while having only $15,000 available in cash.

This creates an “asset-rich but cash-poor” situation.

Without liquidity, unexpected emergencies can become major financial problems.

Real Estate Equity Valuation vs. Spending Power

Property values often inflate net worth dramatically.

Imagine owning:

- Three rental properties

- A valuable primary residence

Your real estate equity valuation may exceed several million dollars.

However:

- Selling property takes time.

- Market conditions may reduce prices.

- Borrowing against equity creates new debt.

High property values do not automatically increase everyday spending power.

Examining Your Liquid Asset Portfolio Value

To understand your financial flexibility, calculate your liquid asset portfolio value.

Include:

- Cash

- Checking accounts

- Savings accounts

- Treasury bills

- Mutual funds

- ETFs

- Public stocks

Exclude:

- Primary residence

- Business ownership

- Collectibles

- Vehicles

- Retirement accounts with heavy withdrawal penalties

Ask yourself:

“How many months could I comfortably live without earning another paycheck?”

This answer often reveals more about wealth than your total net worth.

Which Metric is Better for Retirement Planning?

For retirement, net wealth is generally the more valuable measurement.

Retirement depends on sustainable income—not simply owning expensive assets.

Maintaining a Healthy Debt to Asset Ratio

A growing net worth can hide excessive leverage.

Monitor your debt-to-asset ratio regularly.

Questions to ask:

- Can my investments cover loan payments?

- Am I reducing debt every year?

- How does debt impact my net wealth over the next 20 years?

Healthy leverage supports growth.

Excessive leverage increases financial risk.

How Do Millionaires Calculate Their Total Wealth?

Many wealthy individuals think beyond asset values.

They evaluate:

- Cash flow

- Investment yield

- Asset longevity

- Tax efficiency

- Portfolio resilience

- Business scalability

- Passive income

Instead of asking:

“How much do I own?”

They ask:

“How much financial freedom do my assets create?”

That mindset separates wealth builders from asset collectors.

Modern Investment Portfolio Diversification

Diversification strengthens long-term wealth.

A balanced portfolio may include:

- Domestic stocks

- International equities

- Bonds

- Real estate

- Private businesses

- Cash reserves

- Commodities

- Alternative investments

Non-correlated assets reduce volatility and improve financial stability during market downturns.

How to Convert Net Worth into Wealth for True Financial Stability

Building wealth requires intentional planning rather than simply accumulating assets.

Evaluating Non-Financial Tangible Wealth

Not all valuable assets appear in brokerage accounts.

Examples include:

- Intellectual property

- Copyrights

- Patents

- Professional expertise

- Business systems

- Brand reputation

- Digital businesses

- Licensing income

These assets often generate recurring income for decades.

Mapping Out Generational Wealth Transfer Strategies

True wealth extends beyond one lifetime.

Effective generational wealth transfer strategies include:

- Estate planning

- Family trusts

- Tax-efficient gifting

- Investment education for heirs

- Succession planning

- Diversified family investment portfolios

Building a legacy requires protecting wealth as carefully as creating it.

Recognising the Signs You Are Building Real Net Wealth

You are likely building genuine wealth if:

- Passive income exceeds monthly expenses.

- Emergency savings cover at least six months.

- Debt continues to decline.

- Investments generate consistent long-term growth.

- Financial stress decreases each year.

- Retirement goals remain on schedule.

- Cash flow improves without increasing work hours.

- Your family becomes financially more secure over time.

These indicators matter far more than temporary increases in paper net worth.

Conclusion

Understanding Net Worth vs Net Wealth changes how you evaluate financial success. Net worth offers a useful snapshot of your current financial position, but it doesn’t always reveal whether you can comfortably handle emergencies, retire confidently, or maintain your lifestyle without relying on active income. Net wealth takes a broader perspective by considering liquidity, sustainable cash flow, debt management, income-producing assets, and long-term financial resilience. Rather than chasing impressive numbers on paper, review your personal balance sheet today, strengthen your liquid assets, reduce unnecessary debt, and focus on building lasting financial freedom that provides both stability and peace of mind for years to come.

Frequently Asked Questions (FAQs)

1. How often should I calculate my net worth?

Most financial experts recommend reviewing your net worth every three to six months. Monthly updates can create unnecessary stress because market values fluctuate frequently.

2. Should retirement accounts be included in net worth?

Yes. Retirement accounts are valuable assets and should be included when calculating net worth, although they may not count as liquid assets due to withdrawal restrictions.

3. Can inflation reduce my net wealth even if my net worth increases?

Yes. Rising inflation can reduce your purchasing power. Even if your assets increase in value, your real net wealth may decline if your investments fail to outpace inflation.

4. What is the fastest way to improve net wealth?

Focus on increasing income-producing assets, reducing high-interest debt, maintaining adequate liquidity, investing consistently, and avoiding unnecessary lifestyle inflation.

“Hi, I am Umer Hasib. I am a passionate blogger and content creator who loves exploring human psychology, social behaviors, and personal growth. Welcome to my inner space!”